1950

to present

Establishment of the Federal Fiscal Court in September 1950

Legal protection and legal uniformity as tasks of the Federal Fiscal Court

Copyright: Federal Fiscal Court/Photo Peter-Paul Weiler

With the founding of the Federal Republic of Germany, it became possible once again to establish a supreme tax court with nationwide jurisdiction. According to Article 108(6) of the Basic Law, fiscal jurisdiction is regulated uniformly by federal law.

FFC Act 1950

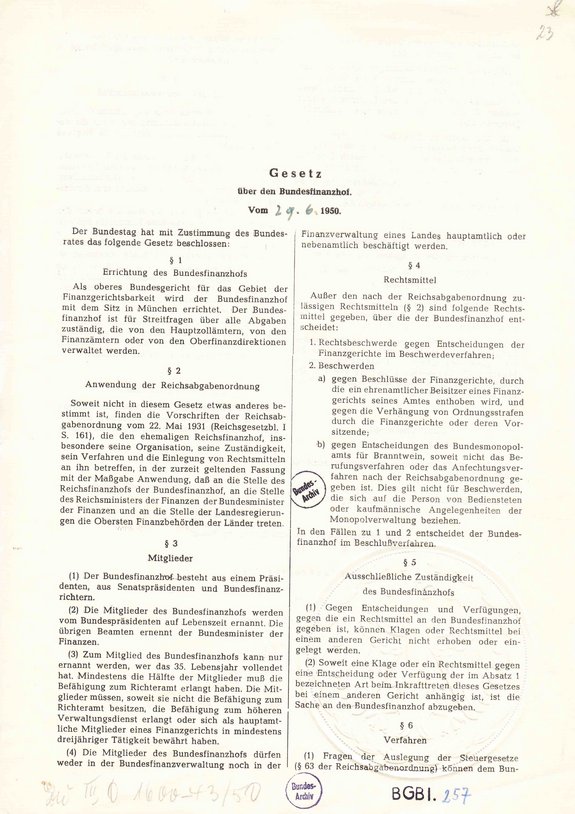

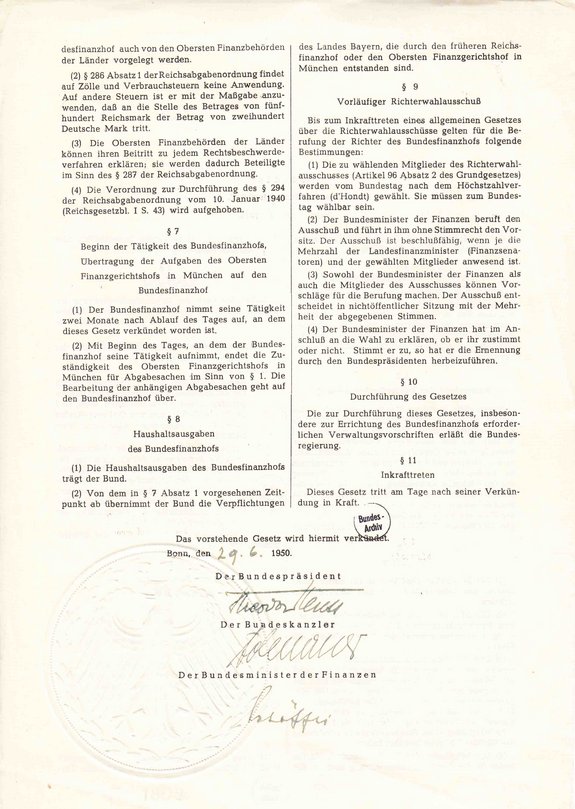

The Federal Fiscal Court was established by the Federal Fiscal Court Act of June 29, 1950 (Federal Law Gazette I 1950, p. 257) and was thus the first of the supreme courts of the Federation referred to in Article 95 of the Basic Law. It commenced its activities on September 1, 1950.

Copyright: Federal Law Gazette I 1950, 257

Copyright: Federal Law Gazette I 1950, 257

Founding members in 1950

During a ceremony marking the establishment of the Federal Fiscal Court, the former president of the Supreme Fiscal Court, Dr. Heinrich Schmittmann, received the certificate of appointment as president of the Federal Fiscal Court from the then Federal President, Prof. Dr. Theodor Heuss.

The political burden on members of the Federal Fiscal Court was a decisive criterion in the election. Seven judges of the Federal Fiscal Court had already served on the Reich Fiscal Court. Some of the elected individuals had also been members of the NSDAP and had been cleared or classified as followers in the denazification process. Later, other former party members were elected to the Federal Fiscal Court. Care was taken to ensure that they did not constitute a majority in a senate. Furthermore, a former member of the NSDAP was not permitted to serve as chair of a senate.

At the beginning, the Federal Fiscal Court had four senates and 19 members—all of whom were male—who had previously been elected by the German Bundestag's Judicial Selection Committee.

Name and location of the Federal Fiscal Court

The name “Federal Fiscal Court” was chosen in reference to the previous name “Reich Fiscal Court”. Munich was retained as the location because the existing building there was suitably equipped and offered an excellently equipped library. Even after the accession of the new federal states in 1990, it remained in Munich. Unlike the other supreme federal courts, for which a move to the new federal states was discussed and in some cases (Federal Administrative Court and Federal Labor Court) also carried out, it was very soon decided that the Federal Fiscal Court would remain in Munich. This had always been the seat of Germany's supreme court for tax and customs disputes.

Copyright: Federal Fiscal Court/Photo Daniel Schvarcz

Expansion to current size

After its establishment, further senates were set up in quick succession: the Fifth Senate in 1952, the Sixth Senate in 1956, and the Seventh Senate in 1958. The need for a new senate only arose again with the creation of the Eighth Senate in 1971. After another 13 years, the establishment of the Ninth Senate became imperative in 1984. The establishment of the Tenth Senate in 1987 and the associated expansion of capacity were a direct response to the rapidly increasing workload of the court. Due to reunification, a significant increase in appeal proceedings was to be expected. For this reason, the budgetary legislator approved the establishment of the Eleventh Senate in 1990.

Copyright: Federal Fiscal Court/Photo Peter-Paul Weiler

Copyright: Federal Fiscal Court/Photo Peter-Paul Weiler

Tax case law since 1950

The Federal Fiscal Court is one of the five supreme courts of the federal government. It is the court of last resort for disputes in the field of tax and customs law, but not for related criminal proceedings, which fall under the jurisdiction of the general criminal courts (with the Federal Court of Justice as the court of last resort). Legal protection by the Federal Fiscal Court is of crucial importance. The reach of the modern tax state is one of the most intensive sovereign interventions in the sphere of freedom of citizens. This intervention affects citizens throughout their entire working lives and is therefore more intensive than other sovereign measures that only affect them in exceptional cases, such as fines, police coercive measures or criminal prosecution. It is therefore all the more important that the sovereign actions of the taxing state are carried out in accordance with the rule of law and are subject to independent judicial review.

Important decisions of the Federal Fiscal Court

Judgment in case X R 33/19 on the 'double' taxation of pensions – Part I

On 19 May 2021, the Federal Fiscal Court laid down precise calculation parameters for determining double taxation of pensions for the first time in its landmark ruling X R 33/19. Although the appeal by the plaintiff – who has been receiving a pension since 2007 with a correspondingly high pension allowance – was unsuccessful, the calculation guidelines of the Federal Fiscal Court indicate that future pensioners are likely to be affected by double taxation of their pensions. However, based on the Federal Fiscal Court's calculation guidelines, it appears that future pensioners are likely to be affected by double taxation of their pensions. This is because the pension allowance applicable to each new cohort of pensioners decreases with each passing year. In many cases, it is therefore likely that in future it will no longer be sufficient to compensate for the portion of pension insurance contributions paid from taxed income.

Judgment in case X R 20/19 on the 'double' taxation of pensions – Part II

On 19 May 2021, the Federal Fiscal Court clarified numerous other contentious issues relating to the problem of so-called double pension taxation in a second ruling (X R 20/19). It not only ruled on the treatment of benefits from voluntary supplementary insurance to the statutory old-age pension and questions relating to the so-called opening clause. It also clarified that, in the case of pensions from private investment products outside the basic provision (in short: private pensions), which – unlike statutory old-age pensions – are only taxed on the respective income portion, there can be no double taxation due to the nature of the system. In addition, it ruled that tax-free pension payments include not only the pensioner's annual pension allowances, but also those of any surviving spouse from their survivor's pension. The appeal by the plaintiffs, who had objected to double taxation of part of the pensions received, was unsuccessful.

Judgment in case IX R 15/20 on the constitutionality of the solidarity surcharge

The solidarity surcharge was not unconstitutional in 2020 and 2021. This was decided by the Federal Fiscal Court in its ruling of 17 January 2023 – IX R 15/20. In their appeal to the Federal Fiscal Court, the plaintiffs argued that the solidarity surcharge violated the Basic Law. They referred to the expiry of Solidarity Pact II and thus of the reconstruction aid for the new federal states in 2019. As a supplementary tax, the solidarity surcharge may only be levied to cover peaks in demand. Its exceptional nature prohibits its permanent levying.

The FFC did not agree with this. With the expiry of Solidarity Pact II and the reform of the federal state financial equalisation system at the end of 2019, the solidarity surcharge has not lost its justification as a constitutionally permissible supplementary tax. A supplementary tax (Art. 106 (1) No. 6 of the Basic Law) has the function of covering additional financial requirements of the federal government without increasing other taxes. This is also possible for longer periods of time. The Act on the Repayment of the Solidarity Surcharge makes it clear that the legislature does not intend to levy it indefinitely, but only for a transitional period. In addition, in the disputed years 2020 and 2021, the federal government still had financial requirements due to reunification. The solidarity surcharge also does not violate the general principle of equality (Art. 3(1) of the Basic Law). From 2021 onwards, due to the increased exemption limits, only those with higher incomes will be subject to the solidarity surcharge. The unequal treatment inherent in this is justified. In the case of taxes such as income tax, and thus also the solidarity surcharge, which are based on the taxpayer's ability to pay, it is permissible to take social considerations into account.

Some of the judges who have been in service since 1950

The following judges had a significant influence on tax law in the Federal Republic of Germany: