1933

– 1945

The Reich Fiscal Court under National Socialism

Tax law in the service of National Socialism

Copyright: Bavarian State Library

The position of the Reich Fiscal Court as an independent third power was steadily and increasingly undermined during the Nazi period. The Reich Fiscal Court was regarded as a department of the Reich Ministry of Finance bound by its instructions. Tax law was placed at the service of the National Socialist worldview. In its jurisprudence, the Reich Fiscal Court discriminated against Judaism, the Church, religious orders and religious societies whose basic orientation contradicted National Socialist ideology.

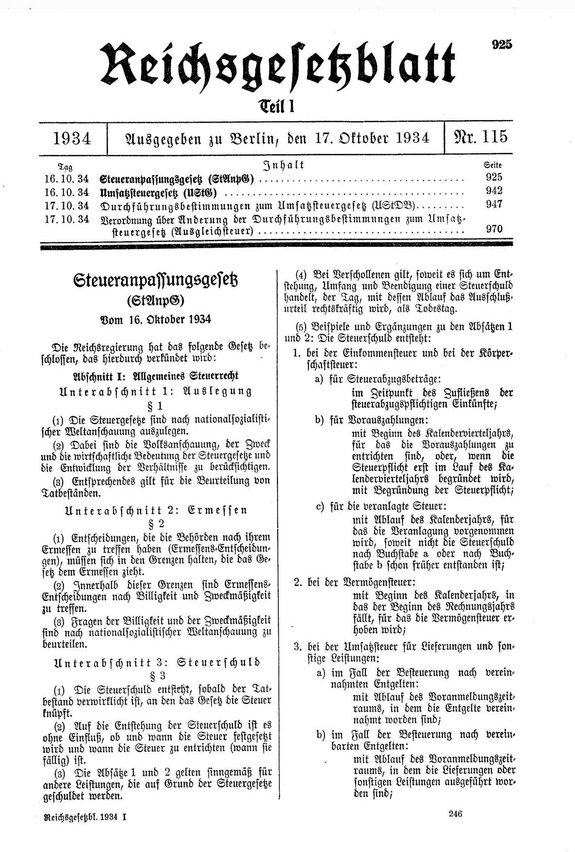

Tax Adjustment Act 1934

From 1933 onwards, the necessary adherence to law and justice was limited. National Socialism had a strong influence on legislation. According to the Tax Adjustment Act, the assessment of legal facts was to be based on the National Socialist world view.

Section 1 of the Tax Adjustment Act of 1934 stated: ‘Tax laws shall be interpreted in accordance with the National Socialist worldview.’ On this basis, the Reich Fiscal Court was to examine whether the regulations that had come into force before 1933 were in line with the National Socialist worldview and, if not, interpret them in accordance with the National Socialist worldview.

Copyright: Austrian National Library

Copyright: Austrian National Library

Reich Fiscal Court as assistant to the Reich Ministry of Finance

The State Secretary in the Reich Ministry of Finance, Fritz Reinhardt, was largely responsible for this. In 1935, he publicly described the role of the Reich Fiscal Court in the following terms: in the National Socialist state, the Reich Fiscal Court was the "assistant to the Reich Minister of Finance in interpreting tax laws and developing tax law in accordance with the principles of the National Socialist world view". The Reich Fiscal Court – which was actually an independent body for the administration of tax law by law – increasingly subordinated itself to the will of the Reich Ministry of Finance.

Copyright: Austrian National Library

Dismissals of judges from the Reich Fiscal Court

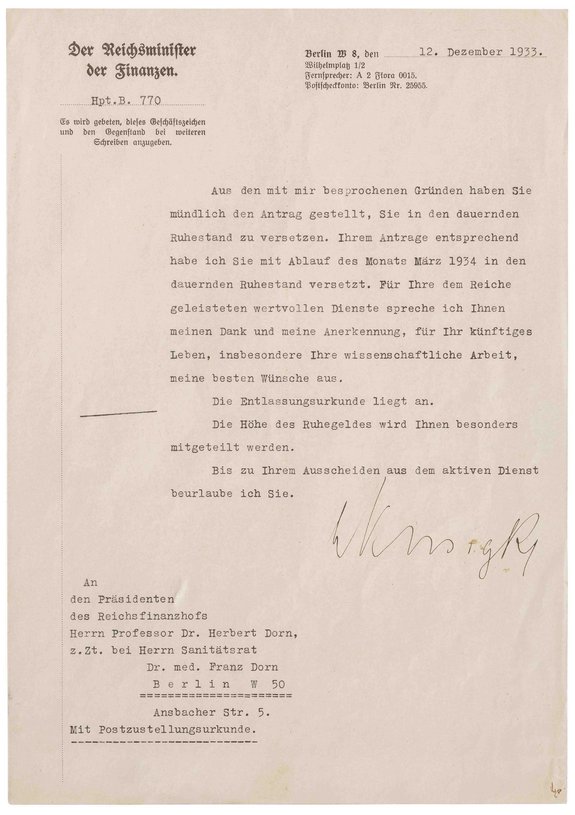

Even before 1935, the National Socialists' seizure of power at the Reich Fiscal Court very quickly led to serious personnel consequences. Under the Law for the Restoration of the Professional Civil Service of 7 April 1933, several members of the Reich Fiscal Court who were either ‘not of Aryan descent’ or ‘politically unreliable’ in the eyes of the new rulers lost their positions.

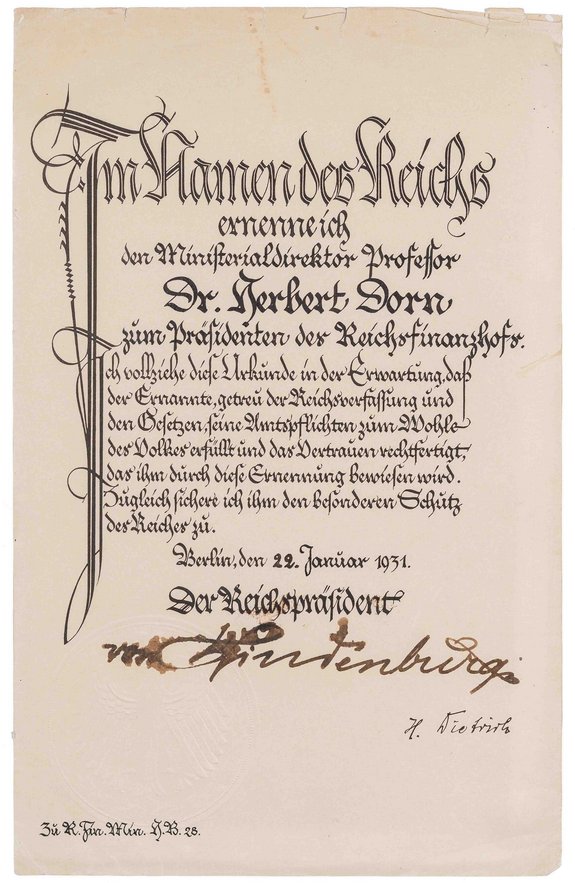

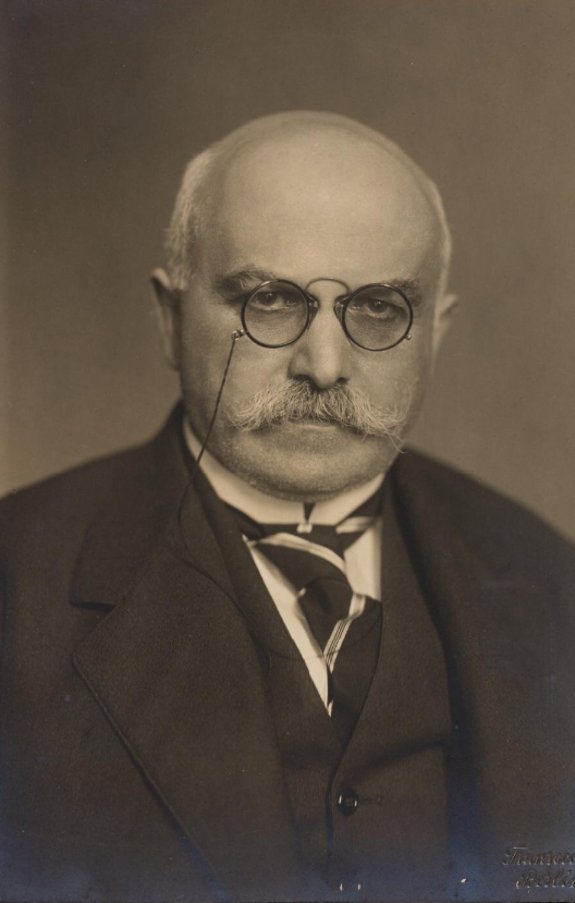

This affected Prof. Dr. Herbert Dorn, who had been president of the court since 1931 and had previously rendered great services to the German Reich in his capacity as a senior ministerial official. The internationally renowned second president of the Reich Fiscal Court was forced out of office because of his Jewish ancestry and emigrated to the USA via Switzerland and Cuba.

Other judges had to leave the court for the same reason. Senate President Heinrich Zapf, who was close to the Centre Party, was also dismissed.

Copyright: Federal Finance Academy

Copyright: Federal Fiscal Court

Copyright: Federal Fiscal Court

Deportations of judges from the Reich Fiscal Court

As a result of the Nuremberg Race Laws, Reich Fiscal Councillors Dr. Franz Oppens, Dr. Rolf Grabower and Robert Wendriner, the latter two highly decorated officers from the First World War, were also forced into early retirement at the end of 1935. Grabower and Oppens were later imprisoned in concentration camps. Grabower survived the Theresienstadt concentration camp. Oppens was murdered in Auschwitz.

Copyright: Federal Fiscal Court

Copyright: Federal Fiscal Court

Copyright: Federal Fiscal Court

Copyright: Rolf Grabower

NSDAP members as judges of the Reich Fiscal Court

The proportion of NSDAP members in the judiciary increased steadily. In addition, more and more members of the Reich Finance Administration were appointed to the Reich Fiscal Court, whereas during the Weimar period, a large number of members of the Reich Fiscal Court had begun their careers in civil and administrative justice.

At almost the same time, however, other people who held leading positions in the financial administration but were considered politically unreliable by the new rulers were ‘shunted off’ to the Reich Fiscal Court, including the later first two presidents of the Federal Fiscal Court, Dr. Heinrich Schmittmann and Dr. Hans Müller. Alexander Prugger, President of the Würzburg state finance president, was also transferred to the Reich Fiscal Court as a Reich Fiscal Judge in 1933 due to political pressure. He was also barred from promotion.

Following the unexpected death of the third court president, Dr. Richard Kloss, who had been in office for less than a year, Dr. Ludwig Mirre was appointed as the fourth court president on 1 April 1935 and presided over the court until the end of the war. The American military administration removed him from office and interned him for several months.

The Reich Fiscal Court becomes a kind of department of the Reich Ministry of Finance.

In 1937, Senate VIa was established in addition to the existing six senates, which was specifically responsible for charitable matters. If a dispute concerned the charitable status of church and Jewish institutions, charitable status was revoked on the basis of Sections 17–19 of the Tax Adjustment Act. Here, the jurisdiction of the Reich Fiscal Court adopted the National Socialist struggle against the church, Judaism, religious orders and religious societies.

The Führer Decree of 1939 made appeals to the Reich Fiscal Court subject to the decision of the Chief Finance President without exception. Among various other measures, this led to the Reich Fiscal Court being effectively eliminated as an independent legal protection body and becoming a kind of department of the Ministry of Finance. In everyday judicial practice, the Reich Fiscal Court appeared as an organ of the National Socialist state. For example, oral hearings began and ended with the so-called German salute, raising the right arm and saying ‘Heil Hitler’.

In the final phase of the Nazi dictatorship, the judicial activities of the Reich Fiscal Court came to a virtual standstill. The office building at 109 Ismaninger Strasse had suffered severe bomb damage in April and June 1944. The war situation led to the relocation of individual senates to smaller towns in rural areas. The number of new cases also declined sharply because the chief finance officers only allowed appeals to the Reich Fiscal Court in exceptional cases. Finally, the surrender of the German Reich in May 1945 marked the end of the approximately 27-year history of the Reich Fiscal Court.

Tax jurisdiction 1933–1945

Assessing the case law of the Reich Fiscal Court during the Nazi regime is complicated by the fact that only around 2,000 of the approximately 30,000 cases dealt with during this period were published. To date, only this small number of decisions has been the subject of academic research. It can be assumed that the judges of the Reich Fiscal Court primarily published those judgements that they considered particularly important. Nevertheless, the analysis of the judicial activities of that time remains incomplete.

In purely numerical terms, judgments that reached comprehensible conclusions in politically uncontroversial cases with reasonable justifications outweigh problematic or clearly unjust judgments. However, judgments based on National Socialist ideology were not a rare exception. Furthermore, injustices committed cannot be justified by purely quantitative considerations.

The Reich Fiscal Court applied tax laws that were themselves unjust and, through its interpretation, often exacerbated the injustice. There is no evidence to suggest that the Reich Fiscal Court was subject to external pressure in this regard. The considerable number of NSDAP members among the judges leads to the conclusion that National Socialist ideologues were also at work.

The large number of highly problematic or clearly unjust decisions against Jewish taxpayers clearly demonstrates that the Reich Fiscal Court did not merely deny Jewish citizens legal protection in individual cases. Rather, with its rulings on the Reich Flight Tax Act and public benefit law, it actively participated in the financial plundering of Jews, which was a fundamental component of the comprehensive persecution measures of the Nazi state.

Examples of tax jurisdiction in the Nazi state

The Reich Flight Tax, introduced in the final phase of the Weimar Republic, was levied on German citizens who emigrated. The tax originally amounted to 25% of their assets. This enormous tax burden was intended to encourage citizens to remain in Germany.

The Reich Fiscal Court applied the Reich Flight Tax to Jewish citizens, even though many of them had been forced to leave their homeland due to Nazi persecution. In its ruling, it glossed over the persecution measures as mere harassment and, contrary to the actual circumstances, assumed that the emigration of Jews was not in the interests of the Nazi state.

The interpretation of individual provisions of the Reich Flight Tax Act by the Reich Fiscal Court led to additional burdens and rendered the tax exemptions provided for by law inapplicable. The result was that ‘Jews must pay under all circumstances’ (quote from Gustav Jahn, 1938). The Reich Flight Tax did not only affect Jewish citizens. All emigrants, including famous writers and scientists who left or were forced to leave Germany because of the political situation, were robbed of a considerable part of their assets by this tax.

In the so-called Third Reich, the regulations governing non-profit status were revised. Tax exemption was granted only if the activity benefited ‘the welfare of the German national community’.

In its rulings, the Reich Fiscal Court not only confirmed the view of the tax authorities that the activities of Jewish organisations were not charitable. It also provided the legal basis for retroactively denying non-profit status for many years. This led to extremely high back tax payments and thus to the destruction of the economic existence of institutions that had previously been recognised as charitable. The non-profit status rulings of the Reich Fiscal Court harmed not only Jewish organisations, but also Christian institutions and religious orders whose basic orientation contradicted National Socialist ideology.

Even outside the scope of the Reich Flight Tax Act and the public benefit regulations, the Reich Fiscal Court openly discriminated against Jewish plaintiffs on the basis of their race and religion in its rulings.

Despite the clear legal situation, it denied a tax concession on the grounds that ‘it would contradict healthy German national sentiment if a Jew were granted the reduced tax rate ...’.

In so-called mixed marriages between ‘Aryans’ and Jews, the Reich Fiscal Court arbitrarily took either the Jewish husband or the Jewish wife as the basis for classification in the most unfavourable tax bracket.

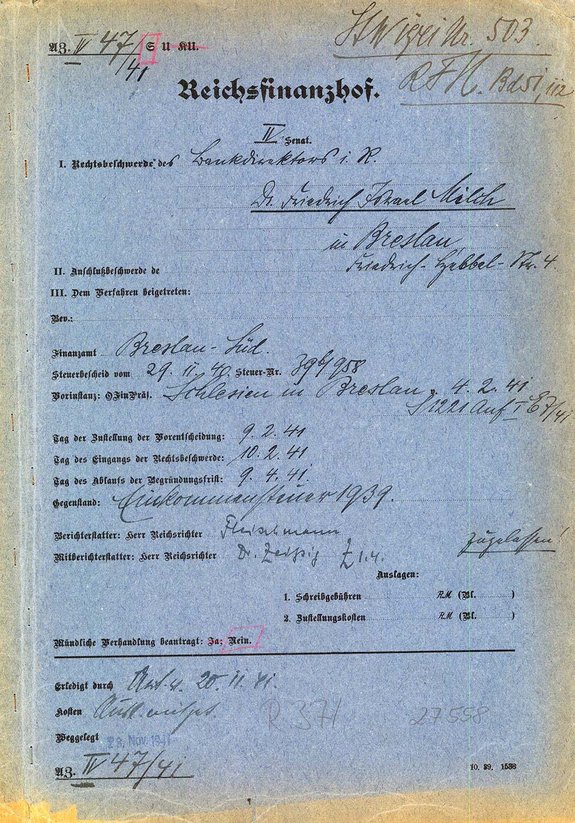

The case Milch

The appeal proceedings of Dr Friedrich Milch, filed with the Reich Fiscal Court under file number IV 47/41, exemplify how the Reich Fiscal Court openly discriminated against Jewish plaintiffs on the basis of their faith in its jurisprudence. In all essential stages of the proceedings, constitutional standards were not met or were blatantly contradicted.

The proceedings also demonstrate the extent to which the Reich Ministry of Finance exerted influence on the Reich Fiscal Court in order to achieve the politically desirable judgement.

Copyright: https://www.bibliotekacyfrowa.pl/dlibra/publication/104249/edition/97317?language=pl

Copyright: German Federal Archives

Some of the judges in service from 1933 to 1945

In 1933, Prof. Dr Herbert Dorn was the Chief President of the Reich Fiscal Court. He was forced to leave office at the end of March 1934. Dorn's successor, Richard Kloß, had been working at the Reich Fiscal Court since 1918. His presidency ended in December 1934. In 1935, Ludwig Mirre was appointed President of the Reich Fiscal Court and remained in office until his dismissal in 1945. From 1935 onwards, the number of judges with NSDAP party membership cards increased steadily.