The case

Milch

An example of discrimination against Jewish plaintiffs in the case law of the Reich Fiscal Court

In 1941, Dr Friedrich Milch's lawsuit is dismissed by the Reich Fiscal Court.

Copyright: German Federal Archives

The legal dispute (Reich Fiscal Court file number IV 47/41) revolved around the question of whether the income received by the taxpayer Dr. Milch was taxable at the standard tax rate or, in accordance with Section 34 of the Income Tax Act in force at the time, only at a reduced tax rate. The Breslau-Süd tax office had refused to apply Section 34 EStG. Dr Friedrich Milch took action against this and lodged an appeal with the Reich Fiscal Court.

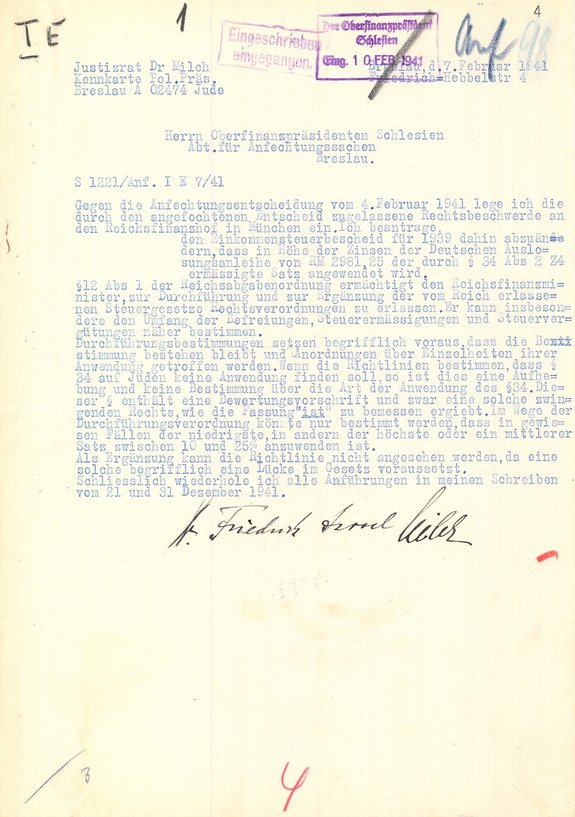

Receipt of the appeal lodged by Dr Friedrich Milch

Justice Councillor Dr Friedrich Milch, a retired bank director, lodged the following appeal against the contestation decision of the Chief Finance Officer of Silesia. The latter had confirmed the tax office's decision that, according to the applicable assessment guidelines, the reduced tax rate did not apply to Jews.

**Explanation:** The legal remedy of appeal corresponds to today's revision. Then as now, the plaintiff must be named with his name and summonable address. The designation of the plaintiff Dr. Milch in the appeal decision and his signature on the appeal show that Jewish taxpayers were discriminated against. In the so-called Third Reich, Jews who had not previously had ‘typically Jewish’ first names had to add “Israel” or ‘Sara’ as an additional first name from 1938 onwards. For this reason, the plaintiff is always referred to as Dr Friedrich Israel Milch throughout the file.

Copyright: German Federal Archives

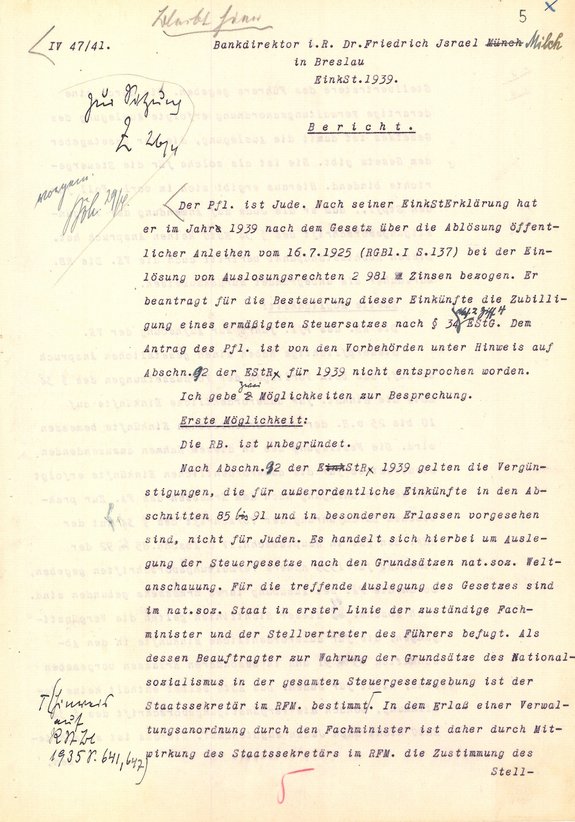

The proposed rulings of Reich Judge Robert Fleischmann

In his report, Reich Judge Robert Fleischmann, appointed as rapporteur by the Fourth Senate of the Reich Fiscal Court to handle the case, outlines two possible ways in which the case could be decided. According to the first option, the appeal is unsuccessful because the assessment guidelines of the Reich Minister of Finance prohibit granting tax concessions to Jews. According to the second option, the appeal is successful because the Income Tax Act provides for tax relief on such interest and does not contain any exemption provisions for Jews.

**Explanation:** Even today, the rapporteur first examines the case and prepares a written report consisting of a proposed decision and a statement of reasons. The first sentence of the report at that time is biased and discriminatory: ‘The taxpayer is Jewish.’ This is because the religion or race of the taxpayer is ‘actually’ irrelevant to the application of Section 34 of the Income Tax Act, both today and at that time.

Copyright: German Federal Archives

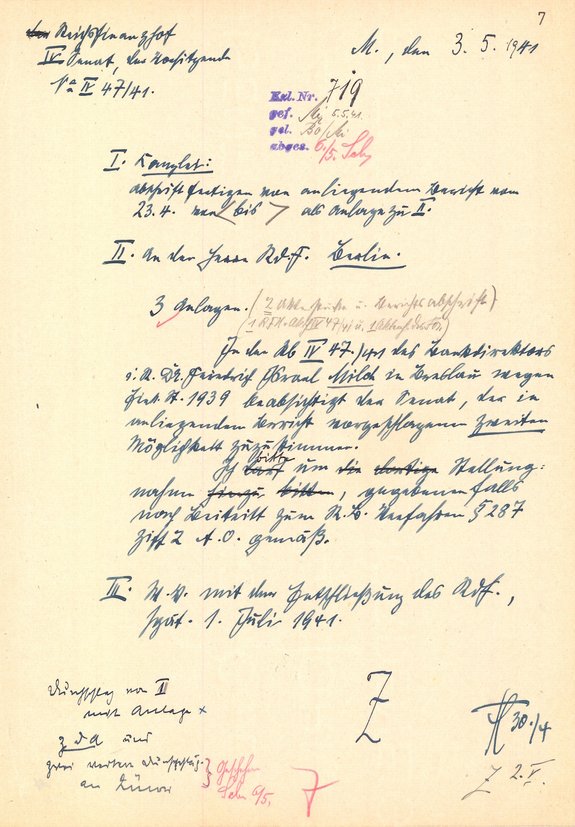

The Reich Fiscal Court agrees with Dr Friedrich Milch

The President of the Senate (Presiding Judge) Dr Kurt Zülow involved the Reich Minister of Finance Johann Ludwig Graf Schwerin von Krosigk and asked him to comment on the report by Reich Judge Robert Fleischmann. Senate President Dr Kurt Zülow went on to say that the Senate intended to ‘approve the second option proposed in the ... report’. The Fourth Senate of the Reich Fiscal Court therefore considers Dr Friedrich Milch's appeal to be well-founded and wishes to uphold it.

**Explanation:** Even under current law, the Federal Fiscal Court can request the Federal Ministry of Finance to join the appeal proceedings and submit a statement on the disputed legal issue. Nevertheless, the involvement of the Reich Ministry of Finance in the Milch case is not an expression of normality under the rule of law. For while the participation of the Reich Minister of Finance in proceedings was rare during the Weimar Republic, the Ministry made frequent use of joining proceedings and issuing statements during the Nazi era in order to exert direct influence on the decisions of the Reich Fiscal Court. In the Milch case, the plaintiff was not informed of the ‘enquiry’ to the Ministry. Nor was he given any opportunity later on to comment on the Ministry's statement. This violated the principle of the right to a fair hearing (Art. 103 Basic Law), which is now enshrined in the Basic Law.

Copyright: German Federal Archives

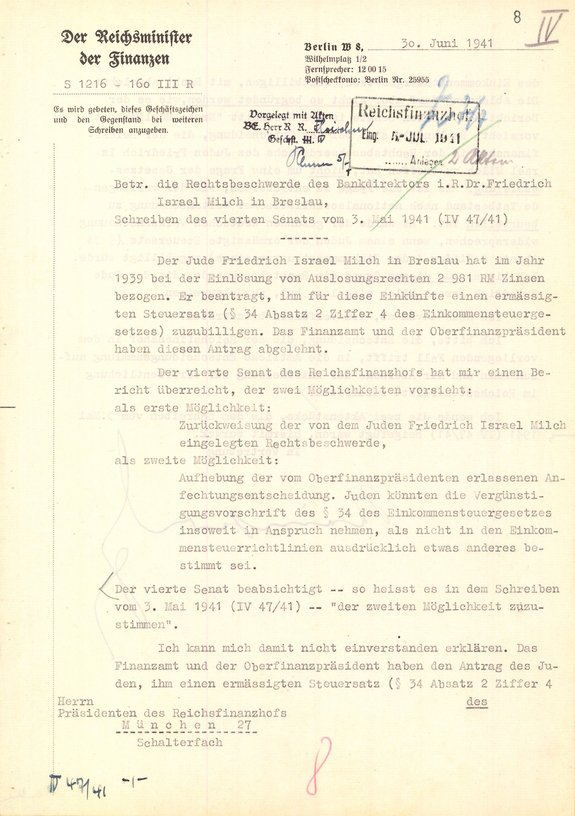

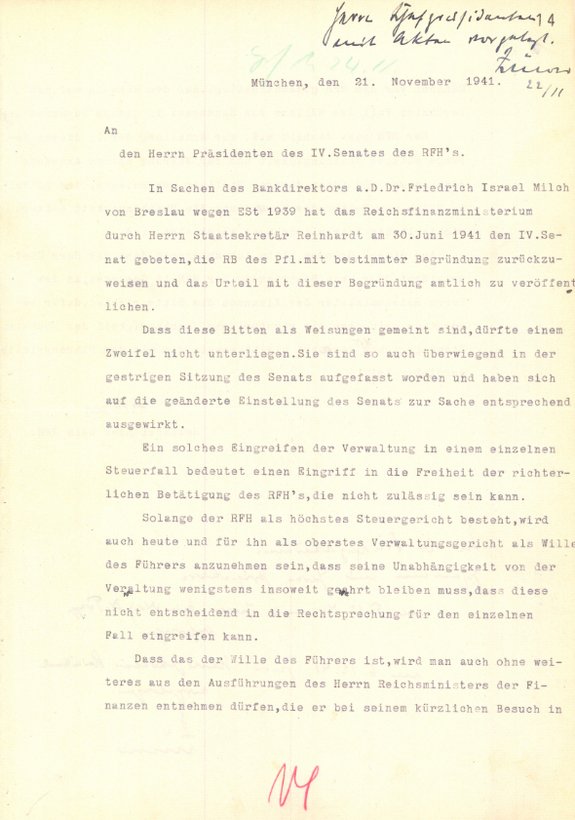

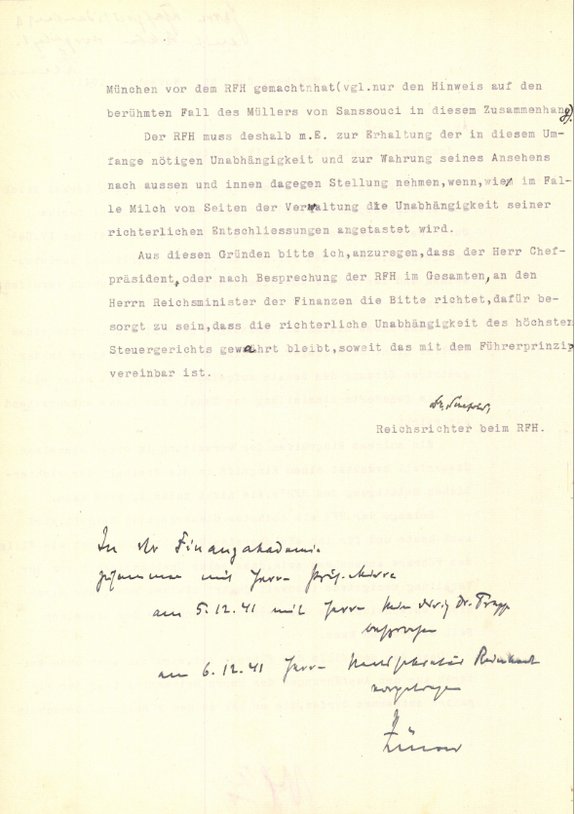

NS State Secretary Fritz Reinhardt intervenes

The following document shows the first page of a two-page reply letter from the Reich Minister of Finance dated 30 June 1941. The letter is signed by State Secretary Fritz Reinhardt. During the Nazi period, Reinhardt was the most influential person in the field of tax law. Fritz Reinhardt states that he ‘cannot agree’ with the Reich Fiscal Court's decision to approve the ‘second option’, i.e. to rule in favour of the plaintiff. He requests that Dr Friedrich Milch's appeal be dismissed. However, the Reich Fiscal Court should not justify this as he himself had considered it to be the ‘first option’. Rather, the decision should be accompanied by a completely new justification, which State Secretary Fritz Reinhardt himself provides in the documented letter. According to this, "it would be contrary to the healthy German national view if a Jew were to be granted the reduced tax rate". Finally, he requests that the decision of the Reich Fiscal Court be included in the official collection of decisions.

**Explanation:** The ‘requests’ made by State Secretary Fritz Reinhardt were in fact orders and were understood as such by the members of the Reich Fiscal Court, as the letter from Reich Judge Dr. Karl Schefold below shows. The judicial independence of the judges of the Reich Fiscal Court, which is now enshrined in Article 97 of the Basic Law and is a cornerstone of our constitutional state, was clearly abolished in 1941.

Copyright: German Federal Archives

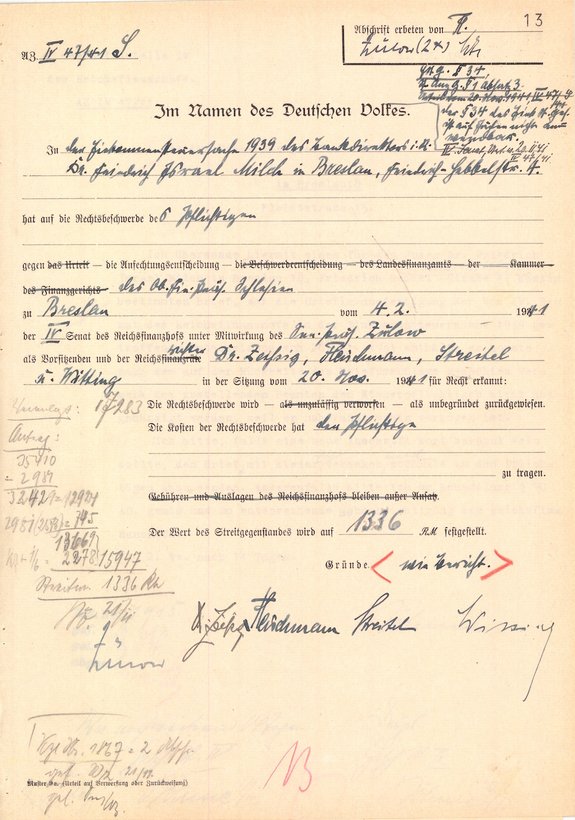

The ruling of the Reich Fiscal Court

The illustration shows the original copy of the judgement of the Reich Fiscal Court of 20 November 1941, in which the Fourth Senate rejected the appeal of Dr. Friedrich Milch. In the reasoning for its decision, the Reich Fiscal Court follows verbatim the written ‘guidelines’ of State Secretary Fritz Reinhardt dated 30 June 1941 (previous illustration). In addition, the Reich Fiscal Court formulated an official guiding principle with which the judgement was later published. It is short and concise: Section 34 of the Income Tax Act does not apply to Jews.

**Explanation:** Article 3(3) of the Basic Law stipulates that no person shall be disadvantaged or favoured because of their ancestry, race, faith or religious beliefs. With its ruling, the Reich Fiscal Court blatantly disadvantaged Dr Friedrich Milch, as well as all other Jewish taxpayers, by denying them the reduced tax rate solely because they were Jewish. It must have been clear to the judges at the time that this was an unjust verdict. After all, they originally wanted to apply Section 34 of the Income Tax Act in accordance with the applicable legal situation. Only historians can assess what consequences it would have had for them if they had not complied with State Secretary Fritz Reinhardt's ‘request’.

Copyright: German Federal Archives

Reich Judge Dr Karl Schefold laments the interference with judicial independence

One day after the Fourth Senate of the Reich Fiscal Court had handed down its ruling in the Milch case, Reich Judge Dr. Karl Schefold addressed the following document to Senate President Dr. Kurt Zülow. He wrote: ‘There can be no doubt that these requests’ – by State Secretary Fritz Reinhardt to reject Dr Friedrich Milch's appeal on specific grounds – ‘are intended as instructions. They were also interpreted as such by the majority of the Senate at yesterday's meeting and had a corresponding effect on the Senate's changed attitude to the matter.’ Reich Judge Dr Karl Schefold complains about the interference with judicial independence inherent in this and asks for the Reich Minister of Finance, Count Schwerin von Krosigk, to intervene.

**Explanation:** The letter from Reich Judge Dr Karl Schefold is one of the most revealing documents in the case file. It clearly shows that, at least in the 1940s, the National Socialist-led Ministry of Finance had sole authority in the field of tax law, that the members of the Reich Fiscal Court were aware of the balance of power, and that they were concerned, if anything, with maintaining the outward appearance of the Reich Fiscal Court as an independent court.

Copyright: German Federal Archives

Copyright: German Federal Archives

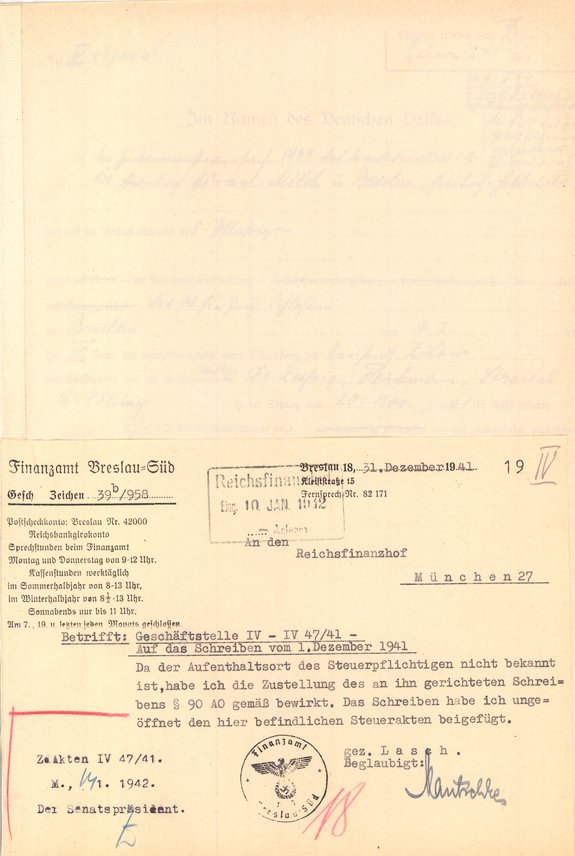

Recipient unknown, moved away – Delivery of the judgement to Dr Friedrich Milch

The following illustration shows the last page of the Milch file. The office of the Fourth Senate had sent Dr Friedrich Milch a copy of the judgement by post. The letter was promptly returned with the note ‘recipient unknown, moved away’. At the request of the Reich Fiscal Court, the Breslau-South tax office therefore arranged for public delivery and added the sealed letter to the tax files.

**Explanation:** Public delivery, which still exists today, does not usually result in the recipient actually receiving the letter from the court. It therefore stands to reason that Dr Friedrich Milch never found out how the Reich Fiscal Court had ruled on his appeal. In order to classify the ‘moved to unknown address’ status, attention must be paid to the date of the judgement. It was issued at the end of November 1941. On 25 November 1941, the first deportation train left Breslau station, carrying around 1,000 Jews to the East, where they were immediately murdered. A few weeks later, on 20 January 1942, top officials of the Nazi state met at the infamous Wannsee Conference in Berlin to organise the ‘final solution’ to the Jewish question.

Copyright: German Federal Archives

Dr. Friedrich Milch emigrates

Dr. Friedrich Milch was not on one of the deportation trains. The 71-year-old, who had persevered for so long because of his “roots in Breslau and German culture,” was able to leave Germany with his wife in October 1941. He emigrated to the United States via Cuba and initially lived in Chicago completely destitute. The Federal Republic of Germany later granted him compensation. He died in 1966 at the age of 96 in a town on Lake Michigan.