1918– 1933

Foundation and development: The Reich Fiscal Court in the Weimar Republic

Pioneering work in the field of modern tax law

Copyright: Federal Fiscal Court

The Reich Fiscal Court shaped modern tax law through its jurisprudence. Its achievements in defining basic tax law concepts and developing special tax law institutions were fundamental and continue to have an impact today. The court succeeded in establishing itself as a generally recognised legal protection authority for citizens.

RFC Act 1918

The Reich Fiscal Court was established by the Reichstag with the ‘Act on the Establishment of an Reich Fiscal Court and on Reich Supervision of Customs and Taxes of 26 July 1918’ (RFC Act).

Copyright: Reich Law Gazette 1918, No. 101

Copyright: Reich Law Gazette 1918, No. 101

Name and location of the Reich Fiscal Court

The name ‘Reichsfinanzhof’ (Reich Fiscal Court) was chosen because it sounded ‘better and more complete’ than “Reichssteuergerichtshof” (Reich Tax Court). The German word ‘finanz’ (in English ‘fiscal’ from the latin word ‘fiscus’, meaning ‘tax authorities’) was also intended to convey that not only tax matters but also other matters relating to levies could be brought before this court. The German word ‘gericht’ (in English ‘court’ ) was omitted because the Reichsfinanzhof (Reich Fiscal Court) was also required to provide expert opinions outside of legal disputes at the request of the Reich Chancellor and the highest financial authorities. This also applied to the Bundesfinanzhof (Federal Fiscal Court) until 1963.

Several cities, including Stuttgart, Berlin, Strasbourg and Leipzig, applied to be the seat of the new court. The Bundesrat, the representative body of the 25 federal states of the German Empire, ultimately chose Munich.

Gustav Jahn becomes the first president of the Reich Fiscal Court

Kaiser Wilhelm II appointed the former Under-Secretary of State in the Reich Treasury, Privy Councillor Gustav Jahn, as Imperial President of the Reich Fiscal Court. He took up his post on 1 October 1918 – without any ceremony due to the war.

Copyright: Property of Heinz von Tengg-Kobligk/Photo Julia Heß

Copyright: Property of Heinz von Tengg-Kobligk/Photo Julia Heß

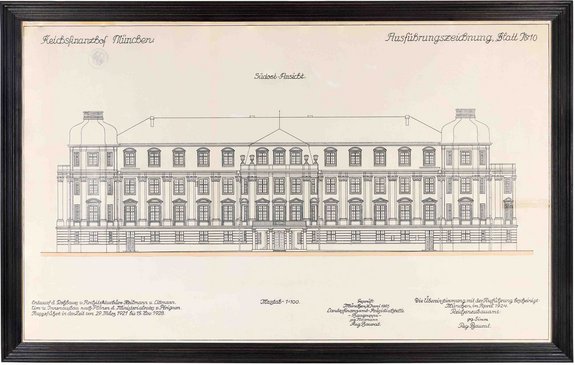

Reich Fiscal Court gets its own office building

In September 1923, the Reich Fiscal Court moved into its new premises at Ismaninger Straße 109 in the Bogenhausen district of Munich, which had been purchased and completed specifically for this purpose and is now used by the Federal Fiscal Court.

More about the building's history

Copyright: Munich I State Building Authority

Copyright: Munich I State Building Authority

Six senates decide

Two senates were formed at the Reich Fiscal Court on 12 October 1918. By 1922, four further senates had been established in quick succession. After a temporary reduction to five senates, the number remained at six until the end of the Weimar Republic in 1933.

The First Senate primarily dealt with corporate income tax, the Second Senate with transfer taxes, the Third Senate with valuation and property tax law, the Fifth Senate with turnover tax law, and the Fourth and Sixth Senates with income tax and trade tax law.

By the time Hitler seized power on 30 January 1933, a total of 65 people, all of them men, had been appointed as judges to the Reich Fiscal Court. They originally held the title of Reich Fiscal Councillor, later Reich Judge. After the end of the monarchy, the law stipulated that judges were to be appointed by the Reich President. The Reich Minister of Finance submitted corresponding personnel proposals.

Applicants had to be at least 35 years old. Qualification as a judge was not mandatory; however, half of the members of the Reich Fiscal Court had to have obtained this qualification. This meant that economists, scientists or civil servants qualified for higher administrative service could also become judges of the Reich Fiscal Court. In fact, the judicial staff consisted mainly of former civil and administrative judges and senior finance officials.

Unlike the judges at the fiscal courts, who were members of the finance administration, the members of the Reich Fiscal Court enjoyed judicial independence. Although the independence of the Reich Fiscal Court was enshrined in law, it was imperfect in that the Reich Minister of Finance was effectively responsible for appointing its members. As the representative of the Reich treasury, he was also a party in most of the court proceedings before the Reich Fiscal Court. The Presidium of the Reich Fiscal Court was in no way involved in the appointment process. All of this already drew criticism from contemporaries.

Reich Fiscal Court reviews judgments of the fiscal courts

The Reich Fiscal Court was the highest adjudicating and decision-making authority for all tax disputes under Reich tax laws. Under the Reich Tax Code, which came into force in 1919, fiscal courts established at the state tax offices were responsible for making decisions in the first instance. Their members were guaranteed judicial independence. However, in addition to administering justice, they also had administrative tasks to perform. In organisational terms, the fiscal courts remained integrated into the state tax offices.

Within the framework of reviewing fiscal court judgements (appeal proceedings), the Reich Fiscal Court was primarily responsible for ensuring that tax laws were applied uniformly throughout the Reich, so that all citizens in the Reich were treated equally under tax law.

As a court of appeal, the Reich Fiscal Court was purely a legal authority. In the appeal proceedings themselves, no new findings of fact, i.e. a review of the facts relevant to the decision, took place. It was the responsibility of the fiscal courts to establish the facts, for example by hearing witnesses or evaluating documents.

Tax jurisdiction 1918–1933

As part of the so-called Erzberger financial and tax reform of 1919/1920, the field of tax law was almost completely overhauled. The numerous new tax laws (e.g. the 1918 Turnover Tax Act, the 1919 Reich Tax Code, the 1919 Inheritance and Gift Tax Act, the 1920 Income Tax Act, Corporation Tax Act of 1920) represented modern tax law and the Reich Fiscal Court, as the court of last resort for the interpretation of this law, had to do pioneering work from then on.

The results of its work during the Weimar Republic were so fundamental that they continue to shape legislation, administration and jurisdiction in the field of tax law to this day.

The ongoing legal achievements of the Reich Fiscal Court include, above all, the emancipation of tax law from civil law, the development and definition of basic tax law concepts, and the formation of special tax law institutions and legal theories.

Examples of pioneering work

The Reich Fiscal Court established, based on the then-existing Section 4 Reich Tax Code, the economic approach. Its significance essentially lay in enabling the interpretation of terms used in tax laws – frequently borrowed from civil law – to be given a tax-law-specific meaning, independent of civil law. This led to the now self-evident understanding that identical terms in different legal provisions do not necessarily have to be interpreted in the same way. Thus, under tax law, a rental arrangement could exist – even contrary to civil law – if the temporary use of a property was based not on a lease agreement but on a usufruct right. The legislator has adopted the economic approach developed by the Reich Fiscal Court in important individual provisions, for example in Section 39 of the German Fiscal Code, which serves as the central attribution rule in tax law (economic ownership").

The application of the economic approach in interpreting the law led to the development of an independent tax-law terminology and thus significantly contributed to the autonomy of tax law as a self-standing sub-field of law, distinct from civil law. However, the economic approach also entailed problems, as it could be used to interpret the written law quite freely.

Numerous terms in modern tax law that are taken for granted today can be traced directly back to the case law of the Reich Fiscal Court between 1918 and 1933. The terms coined and the detailed definitions provided by the Reich Fiscal Court were often so concise that legislators adopted them as legal definitions in numerous individual tax laws. For example, the basic tax law terms ‘business expenses’ (Section 4 (4) EStG), ‘partial value’ (Section 6 (1) No. 1 Sentence 3 EStG) and ‘remuneration’ (Section 10 (1) Sentence 2 UStG) can be traced directly back to decisions of the Reich Fiscal Court.

The same applies to other terms that have become an integral part of tax law terminology: beneficial ownership, hobby, economic asset, hidden profit distribution, reserve for replacement purchases, restructuring profit, fiscal unity, and so on.

The Reich Fiscal Court also made lasting contributions to the development of special tax law institutions and legal theories. These were created in the course of judicial development of the law and were later enshrined in law and further developed in many cases.

The income tax group, first codified in 1969 in Section 7a of the Corporation Tax Act, can be traced back to the group theory developed early on by the Reich Fiscal Court. Despite legal independence, a company could be a mere subsidiary of another tax entity, with the result that the profit generated by the subsidiary was attributed to the other tax entity (parent company) and was taxable by the latter. In turnover tax law, the Reich Fiscal Court's subsidiary theory led to the elimination of the taxability of internal transactions between subsidiaries and parent companies.

The conversion of companies regularly leads to the disclosure of hidden reserves. The resulting threat of profit taxation can complicate or even prevent the economically sensible restructuring of companies. This prompted the Reich Fiscal Court to develop tax-relieving principles of jurisprudence, which significantly influenced legislators when they first comprehensively regulated conversion tax law in 1957.

With a multitude of decisions and expert opinions on the concept of profit and profit determination, the early Reich Fiscal Court broke new ground in tax law. In its case law, it gradually developed a system of accounting-based profit determination (balance sheet tax law). The Reich Fiscal Court thus became the father of the tax balance sheet and, with its case law, also exerted considerable indirect influence on commercial law.

The judges from the very beginning

In addition to Chief President Gustav Jahn, the Reich Fiscal Court initially consisted of a Senate President, i.e. a presiding judge, and seven Reich Fiscal Councillors, who together formed two senates. The Emperor had appointed the following gentlemen: